Financial markets in 2025

In the reporting year 2025, previously high inflation rates worldwide showed a downward trend, even though the central banks' target ranges had not yet been fully achieved. U.S. trade policy - characterised by higher tariffs - created significant uncertainty in the markets and the real economy from April onwards, leading to a pronounced depreciation of the U.S. dollar.

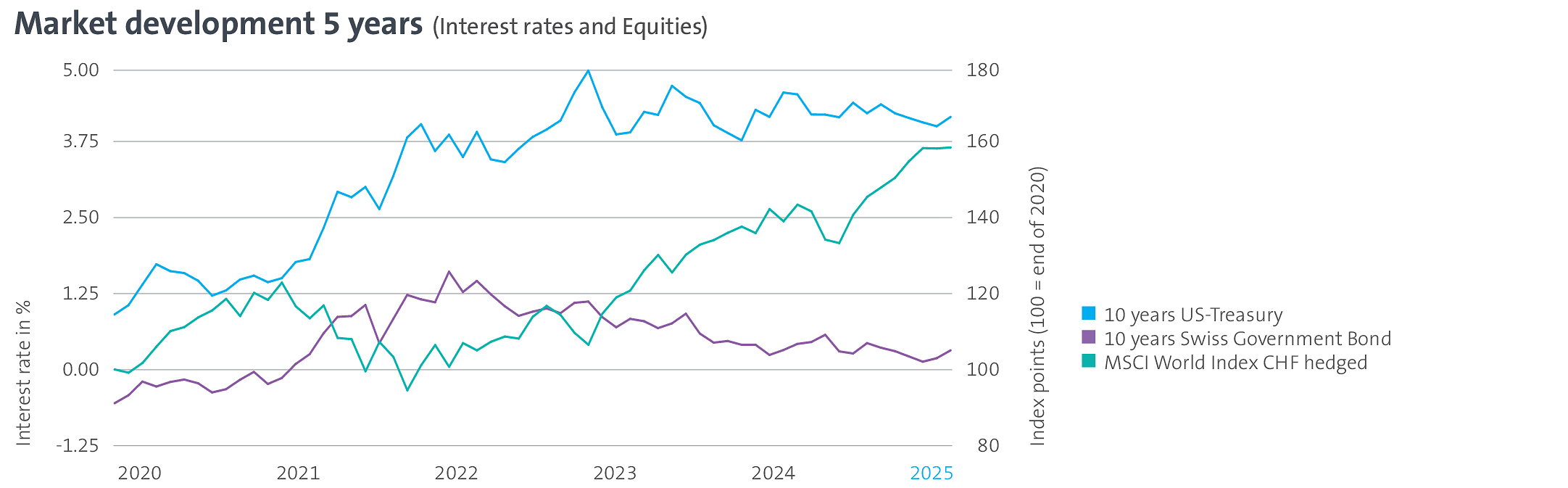

Global economic output grew moderately and several central banks adopted a more accommodative policy stance. In Switzerland, the Swiss National Bank lowered its policy rate by 0.5 percentage points in the first half of the year. As a result, after only three years of positive interest rates, Switzerland returned to a zerointerestrate environment again. The Swiss 10-year yield fluctuated over the course of the year, but closed at the previous year's level of just over 0.3% (see purple line in the chart). In the US, policy rates were lowered by 0.75 percentage points by year end as a result of uncertain trade policy. The 10-year yield fell by 0.4 percentage points over the course of the year (see light blue line in the chart).

This market environment led to a generally flat price performance for Swiss bonds, while global bonds in local currency generated positive returns. Corporate Credit spreads remained largely unchanged. Broad equity markets recorded price gains worldwide and across all regions. A decisive element was the treatment of USD currency risk: the global equity index achieved a return of around +14% when hedged back to the Swiss franc (see green line in the chart) and around +6% without hedging.

Geopolitical tensions, high government debt, and increasing discussions about the stability of democratic systems caused additional uncertainty. The price of gold rose significantly. Real estate investments in Switzerland benefited from decreasing discount rates and generated price gains, while global real estate investments posted slightly positive quarterly returns for the first time after several challenging years. Private market investments generated modest valuation gains. For the third year in a row, their returns lagged significantly behind those of listed equities.